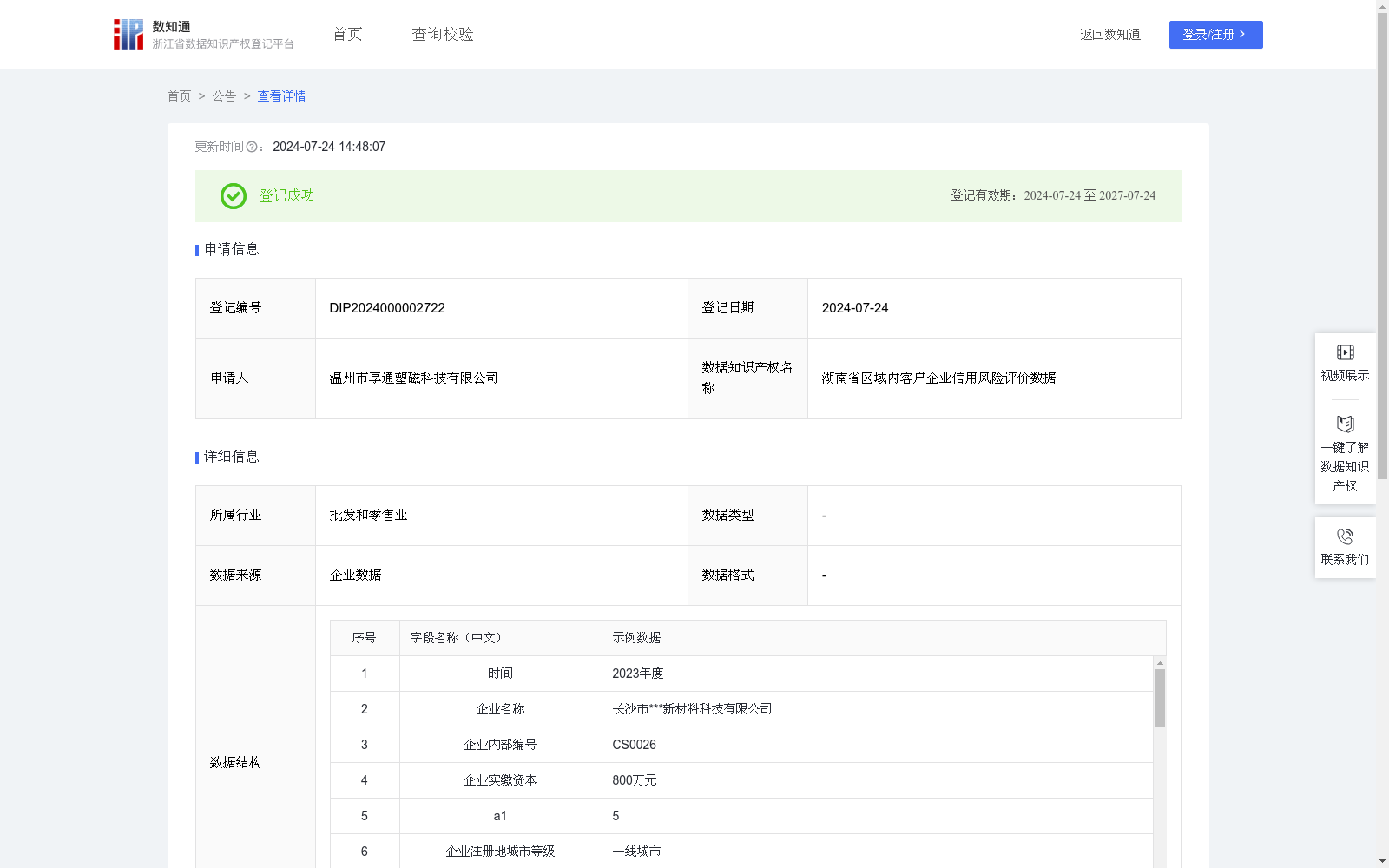

湖南省区域内客户企业信用风险评价数据

收藏浙江省数据知识产权登记平台2024-07-24 更新2024-07-25 收录

下载链接:

https://www.zjip.org.cn/home/announce/trends/41735

下载链接

链接失效反馈官方服务:

资源简介:

材料制造行业普遍存在交易前先付20至30%的定金,等客户收到全部货物再付其余尾款,会存在有客户迟迟拖欠尾款的情况发生。企业信用风险在经济管理领域中起着非常重要的作用,可以帮助本行业所有企业识别和评估客户企业的信用风险,从而避免因客户违约而造成的损失。通过评价客户的信用风险等级,对于评优秀的企业,本行业所有企业可以放心合作或者降低定金比例促进双方交易量,而对于评良好的企业,本行业所有企业需要与客户企业维持在30%左右的定金比例上合作,而对于评不及格的企业,本行业所有企业一定需要与客户企业在50%以上的定金比例上才能合作,从而避免因客户违约而造成的损失。1.对近一年合作的企业采集相关数据。2.算法规则:(1)a1(注册资本≥1亿元加20分,在0.1至1亿元加10分,其余都只加5分)(2)a2(一线城市加20分,二线加10分,其余加5分)(3)a3(员工≥100人加15分,30至100人加8分,其余加3分)(4)a4(知识产权总数≥25个加15分,15-25个加8分,其余加5分)(5)a5(国家级荣誉加20分,省级荣誉加15分,市级荣誉加8分)(6)a6(企业有≥20司法诉讼减10分,有5至20条减5分,5条以下加5分)(7)a7(凭主观打0至10分)(8)a8(企业等级在A和B级的加15分,企M级的加8分,C和D级的减2分)(9)a9(与本行业所有企业有≥3违约的减10分,有1或者2次违约的减5分,0次违约的加15分)。3.计算信用风险值A=(a1+a2+......a9)*k1,k1不同省份值不同,浙江省k1值为1.08。4.评价企业信用风险等级,A大于等于85分为优秀,65-85分为良好,小于等于65分为不及格,从而帮助本行业所有企业识别和评估客户企业的信用风险,从而避免因客户违约而造成本行业所有企业的损失。

In the material manufacturing industry, it is a standard transaction practice to require a 20% to 30% upfront down payment, with the remaining final balance to be settled after the client receives the full shipment. However, this practice often exposes enterprises to the risk of clients delaying payment of the outstanding balance. Enterprise credit risk is of paramount importance in the field of economic management, as it enables all enterprises within the industry to identify and assess the credit risk of their client enterprises, thereby mitigating losses caused by client defaults.

By evaluating the credit risk rating of client enterprises, all industry enterprises can adopt corresponding cooperation strategies: cooperate with rated-excellent clients with full confidence, or reduce the down payment ratio to boost transaction volume; maintain a down payment ratio of approximately 30% when cooperating with rated-good clients; and require a down payment ratio of no less than 50% before cooperating with rated-fail clients, so as to avoid losses caused by client defaults.

1. Data Collection: Gather relevant operational data from enterprises that have cooperated with the industry entities over the past year.

2. Algorithm Rules:

(1) a1: +20 points if the registered capital is ≥ 100 million RMB, +10 points if the registered capital is between 10 million and 100 million RMB, and +5 points for all other cases.

(2) a2: +20 points if the enterprise is located in a first-tier city, +10 points if located in a second-tier city, and +5 points for all other cases.

(3) a3: +15 points if the number of employees ≥ 100, +8 points if the number of employees is between 30 and 100, and +3 points for all other cases.

(4) a4: +15 points if the total number of intellectual property rights ≥ 25, +8 points if the total number is between 15 and 25, and +5 points for all other cases.

(5) a5: +20 points for national-level honors, +15 points for provincial-level honors, and +8 points for municipal-level honors.

(6) a6: -10 points if the enterprise has ≥ 20 judicial lawsuits, -5 points if having 5 to 20 judicial lawsuits, and +5 points if having fewer than 5 judicial lawsuits.

(7) a7: Subjectively scored from 0 to 10 points.

(8) a8: +15 points if the enterprise's credit rating is Grade A or B, +8 points if Grade M, and -2 points if Grade C or D.

(9) a9: -10 points if the enterprise has ≥ 3 defaults with all industry enterprises, -5 points if having 1 or 2 defaults, and +15 points if having 0 defaults.

3. Credit Risk Score Calculation: The total credit risk score A is calculated as A = (a1 + a2 + ... + a9) * k1, where k1 varies across different provinces. The k1 value for Zhejiang Province is 1.08.

4. Credit Risk Rating Classification: Classify enterprises into three tiers based on score A: Excellent (A ≥ 85), Good (65 ≤ A < 85), and Fail (A ≤ 65). This framework helps all enterprises in the industry identify and evaluate the credit risk of their client enterprises, thus avoiding losses caused by client defaults.

提供机构:

温州市享通塑磁科技有限公司

创建时间:

2024-07-05

搜集汇总

数据集介绍

特点

该数据集名为'湖南省区域内客户企业信用风险评价数据',包含13932条记录,每年更新一次。数据集来源于企业数据,主要应用于材料制造行业,用于评估客户企业的信用风险。通过特定的算法规则,计算企业的信用风险值,并根据评分结果将企业信用风险等级分为优秀、良好和不及格,帮助企业决策合作策略。

以上内容由遇见数据集搜集并总结生成