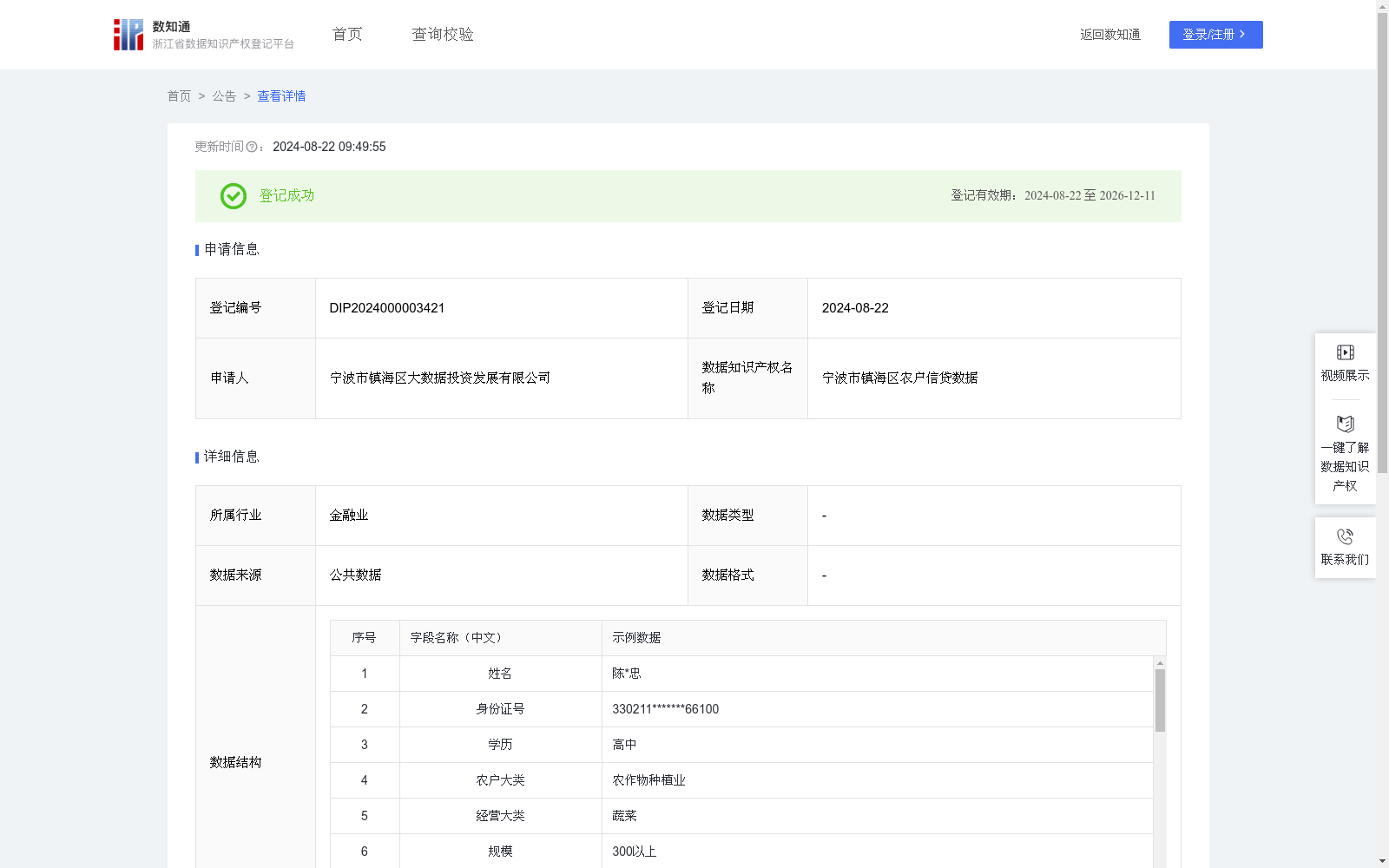

宁波市镇海区农户信贷数据

收藏浙江省数据知识产权登记平台2024-08-22 更新2024-08-23 收录

下载链接:

https://www.zjip.org.cn/home/announce/trends/53875

下载链接

链接失效反馈官方服务:

资源简介:

通过搭建“信用惠农”应用,运用多方安全计算等技术手段结合公共数据、农户数据融合,推动金融机构联合建模,实现相关数据采集、清洗、计算、分析,完成数据产品搭建,并在农户贷款准入、贷款授信额度等流程中进行综合评测使用,加强涉农信用信息共享和应用,最终对优质农户提供优惠政策,提高贷款额度、降低贷款利率。解决农户贷款难、额度低问题,结合农业小额贷款贴息政策,做好三农扶持,进一步探索、创新农业贷款,加大农户信用贷款投放力度。1、贷前准入模型: 数据输入要素:农户数据:负面信息; 计算模型:农户数据-负面信息中存在以下十一项中两项及以上,拒绝(家庭成员欠债不还或有赖账;家庭成员品德较差;家庭成员存在民间借贷;家庭成员涉嫌赌博行为;邻里关系紧张;与村民关系不融洽;存在不遵守村规民约;不配合组织工作开展) 数据输出:是/否给予准入。 2、预授信用评估模型: 数据输入要素:公共数据:中华人民共和国机动车行驶证、公共缴费信息、公共信用欠税信息;农户数据:基本情况数据、资产数据、经营类型数据、经营规模数据、负面信息。 计算模型:学历得分A:按不同学历给于不同的评价区间。 负面信息得分B:每有一项负面M分。 公共缴费分C:有公共欠费一次N分 公共信用欠税分D:每欠税一次L分。 机动车分E:每有一辆机动车S分。 按照预设的模型计算信用得分=A*权重-B*权重-C*权重-D*权重+E*权重 数据输出:根据评分对农户进行分级分类,分为ABCD档,根据农户档位给与不同的可贷额度。 3、贷后风险监测模型: 计算模型:定时对农户进行授信模型再次评估,若农户相较之前分值的幅度超出设定。 数据输出:农户分数下降,存在风险。

By constructing the "Credit for Farmers and Agriculture" application, leveraging technologies including Secure Multi-Party Computation (SMPC) to integrate public data and farmers' data, promoting joint modeling among financial institutions, and completing full-process data collection, cleaning, computation and analysis to build data products, this system conducts comprehensive evaluations in processes such as farmers' loan access eligibility and credit quota determination. It strengthens the sharing and application of agriculture-related credit information, finally provides preferential policies for high-quality farmers including increased loan amounts and reduced loan interest rates, addresses the issues of difficult loan access and low loan quotas for farmers, combines with the agricultural micro-loan interest discount policy to support agriculture, rural areas and farmers, further explores and innovates agricultural loan products, and increases the issuance of farmers' credit loans.

1. Pre-loan Eligibility Model

- Data Input Factors: Farmers' data: Negative information

- Calculation Model: Reject the application if there are two or more of the following 11 items in the family members' negative information of farmers: (family members fail to repay debts or have bad credit records; family members have poor moral character; family members engage in private lending; family members are suspected of gambling; tense neighborhood relations; poor relations with villagers; failure to comply with village regulations; failure to cooperate with organizational work)

- Data Output: Yes/No for granting loan eligibility

2. Pre-granting Credit Assessment Model

- Data Input Factors: Public data: People's Republic of China Motor Vehicle Driving License, public payment records, public credit tax arrears information; Farmers' data: basic situation data, asset data, business type data, business scale data, negative information

- Calculation Model:

1. Academic Qualification Score A: Different evaluation intervals are assigned based on different academic qualifications

2. Negative Information Score B: Deduct M points for each negative information item

3. Public Payment Score C: Deduct N points for each public arrearage record

4. Public Credit Tax Arrears Score D: Deduct L points for each tax arrearage record

5. Motor Vehicle Score E: Add S points for each motor vehicle

6. Preset credit score calculation formula: Credit Score = A*weight - B*weight - C*weight - D*weight + E*weight

- Data Output: Classify farmers into grades A, B, C, D according to their credit scores, and allocate corresponding loan quotas based on the grade

3. Post-loan Risk Monitoring Model

- Data Input Factors: N/A

- Calculation Model: Regularly re-evaluate farmers using the pre-built credit granting model. If the deviation between a farmer's current score and previous score exceeds the preset threshold

- Data Output: A drop in the farmer's score indicates potential credit risks

提供机构:

宁波市镇海区大数据投资发展有限公司

创建时间:

2024-07-17

搜集汇总

数据集介绍

特点

宁波市镇海区农户信贷数据包含519条记录,每日更新,涵盖农户基本信息、经营情况、负面信息及信用评分等字段,用于信贷准入、授信评估和风险监测,支持金融机构为农户提供贷款服务。

以上内容由遇见数据集搜集并总结生成